www.lucid-is.com/wp-content/uploads/2018/06/SUSHIExplan.pdf

S.49, 50 ff.

"The Scheme is not approved

2.2 If the Scheme is not approved and the Alternative Exit Financing is unsuccessful, Mattress Firm would find itself in a precarious position which could lead to Chapter 7 proceedings or an equivalent “free-fall” within a failed Chapter 11.

2.3 In a hypothetical Chapter 7 case, which is, in effect, an insolvent liquidation, the Scheme Creditors are not expected to receive any return from SUSHI’s indirect shareholding in Mattress Firm, Inc. (the principal operating entity of Mattress Firm), which is held indirectly by SUSHI through a series of wholly-owned holding companies. This is primarily because:

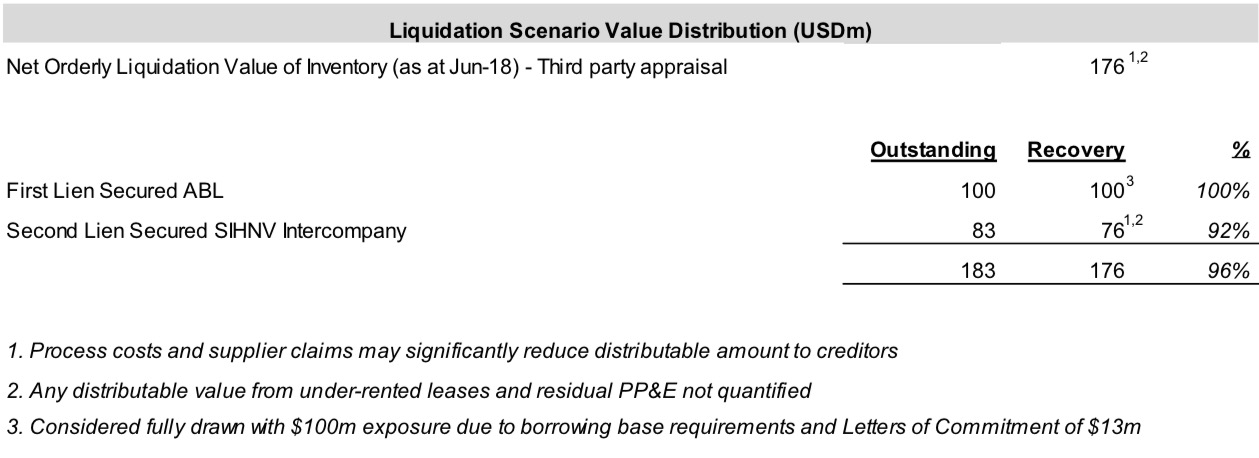

2.3.1 the realisable liquidation value for Mattress Firm is largely based on inventories such as mattresses held for retail sales;

2.3.2 based on third-party analysis, Mattress Firm’s inventories had a net orderly liquidation value (i.e., the estimated value that would be realised via a controlled liquidation process in an accelerated timeframe, as opposed to an ordinary trade sale which would realise in excess of the current carrying cost on the balance sheet) of approximately U.S.$176m in June 2018 (this is not considered to have changed materially since); this is similar to the current level of Mattress Firm’s secured debt of approximately U.S.$183m;

2.3.3 any value achieved from an orderly liquidation will not be wholly distributable to creditors given other potential costs such as trade suppliers who may purport to retain title over inventories and other miscellaneous costs associated with process; and

2.3.4 whilst there are other potential sources of distributable value (e.g. under-rented leases and any residual property, plant and equipment), it is not possible to assume any material value from them.

2.4 As such, it is highly likely that Mattress Firm’s second ranking secured creditor would face a shortfall as regards its lending as illustrated in the table below. This illustrative shortfall would likely be exacerbated further by other potential costs such as supplier claims (e.g. retention of title) and other miscellaneous costs associated with the process. This would mean that there would be no value available to Mattress Firm’s unsecured creditors, let alone equity value for SUSHI and therefore the Scheme Creditors."

Wer das ließt stimmt dem SUSHI Scheme leichter zu ;-)

(Verkleinert auf 44%)