Das globale Finanzsystem steht 2008 vor dem Zusammenbruch

LEAP/E2020 warnt: Das globale Finanzsystem steht 2008 vor dem Zusammenbruch

- Pressemitteilung des GEAB vom 18. Dezember 2007 –

Der GEAB ist noch kein Jahr alt und hat sich dennoch schon weltweit als Informationsbrief der Entscheidungsträger in Politik und Wirtschaft durchgesetzt. Jeden Monat präsentiert das GlobalEuropa Antizipations-Bulletin Ihnen Analysen über den Zerfall der Weltordnung der Nachkriegszeit und seine Konsequenzen für die Weltpolitik, sowie weitreichende Ratschläge für Ihre politischen, wirtschaftlichen und finanziellen Entscheidungen.

Wie vorhergesagt frisst sich die Aufprallphase (1) der weltweiten umfassenden Krise weiter in die Wirtschaft und die Finanzmärkte hinein und führt zu einer raschen Verschlechterung der Situation insbs. an den Finanzmärkten : Unsere Forscher gehen davon aus, dass 2008 das gegenwärtige globale Finanzsystem zusammen brechen wird.

Die Indikatoren, die uns ermöglichen, den Ablauf der Krise zu verfolgen, weisen darauf hin, dass in den nächsten Monaten nicht nur mit Konkursen von großen und vielen kleinen Banken in den USA und etwas später auch in anderen Ländern zu rechnen ist (wir schrieben darüber ausführlich in der 19. Ausgabe des GEAB). Vielmehr gehen wir davon aus, dass das gesamte internationale Finanzsystem auseinander zu brechen droht.

Heute schafft nicht einmal mehr eine konzertierte Aktion der großen Zentralbanken, die Liquiditätsengpässe auf den Finanzmärkten aufzulösen ("credit crunch"). Weiterhin befindet sich die US-Wirtschaft in Rezession und der Dollar steht vor dem Kollaps; damit bröckeln die zwei historischen Pfeiler, die bisher das gegenwärtige internationale Finanzsystem trugen. Heute fehlt es den internationalen Finanzmärkten an der verbindenden Klammer, die die jedem System immanenten widerstreitenden Interessen entgegen wirken konnten.

Wir sind heute in einer Situation, in der auch die besten Zentralbanker und die größtmöglichen Interventionsmaßnahmen nur noch versagen können. Das Zeitfenster für mögliche korrigierende Eingriffe hat sich mit Ende des Sommers 2007 geschlossen. Nach unserer Auffassung sind wir heute Zeugen einer Entwicklung, in der die unterschiedlichen Interessen der verschiedenen Komponenten des internationalen Finanzsystems dessen Fortbestand gefährden.

Als Beleg für diese These genügt es, den Versuch der US-Zentralbank zu analysieren, im Zusammenspiel mit den anderen großen Zentralbanken die Versorgung der Finanzmärkte mit US-Dollar (2) sicherzustellen. Dieser Versuch konnte nur mit einem Fehlschlag enden. Es ging in erster Linie darum, das Vertrauen in die Finanzmärkte mit zwei Maßnahmen zu restaurieren:

1. Indem der Eindruck erweckt werden sollte, die großen Zentralbanken zögen in ihrem Kampf zur Beseitigung der Liquiditätsengpässe an einem Strang, sollte dem heute praktisch zum Erliegen gekommenen Geldmarkt zwischen den Banken wieder auf die Beine geholfen werden.

2. Den großen, in Liquiditätsschwierigkeiten befindlichen Banken wurde die Möglichkeit verschafft, sich ohne Kenntnis der übrigen Marktteilnehmer bei den Zentralbanken mit US-Dollar zu versorgen; als Sicherheiten für diese Kredite durften sie überbewertete Aktiva hinterlegen, da sie nach dem Marktpreis von vor vielen Monaten bewertet wurden, obwohl diese Preise heute sicherlich nicht mehr zu erzielen wären (3).

Natürlich war die Restaurierung des Geldmarkts zwischen den Banken das prioritäre Anliegen dieser konzertierten Aktion der großen Zentralbanken; denn kurzfristige Kredite für Banken, die am Rand des Konkurses stehen, können das letztendliche Ergebnis nur um einige Monate verzögern, nicht aber verhindern.

Heute ist jedoch schon sicher, dass dieses Ziel nicht erreicht wurde (4). Denn der LIBOR (London interbank offered rate), der Referenzzinssatz des Geldmarkts der Banken und damit verläßlicher Indikator für dessen Zustands, verharrt auf seinem sehr hohen Niveau (5). Und die Tatsache, dass als Folge der Meldung über die konzertierte Aktion der Zentralbanken die Aktienkurse abstürzten, ermöglicht einen sehr guten Einblick in die pessimistische Stimmung an den Finanzmärkten: Die Händler und Investoren schöpften aus der zur Schau gestellten "bonne entente" der Zentralbanken nicht Zuversicht für ein baldiges Ende der Kreditkrise. Vielmehr interpretierten sie es als Eingeständnis, dass die finanzielle Situation der großen US-Banken viel schlimmer ist als noch vor einigen Monaten eingeräumt (6).

Konzentration von Finanzderivaten bei allen US-Geschäftsbanken zum 30.09.2007 - Quelle Federal Deposit Insurance Corporation (FDIC) - Kommentar: Sieben Finanzinstitute (7) konzentrieren 98% der Gesamtsumme, also 155 400 Milliarden USD, während 929 andere

Vor einigen Monaten war der US-Zentralbank die Kontrolle über die Entwicklung der Leitzinsen entglitten, wie wir in der 16. Ausgabe des GEAB beschrieben; nunmehr hat sie einen weiteren wesentlichen Machtverlust erlitten: Zum einen hat sie das Vertrauen der Investoren und Händler in ihre Fähigkeit, die Märkte zu steuern (8), verloren, zum anderen die Macht eingebüßt, die anderen großen Zentralbanken für ihre Ziele einzuspannen. Damit kann sie heute nicht mehr die Rolle als alleiniger Steuermann des internationalen Finanzsystems ausüben, die ihr nach dem Ende des 2. Weltkriegs und dank der Verträge von Bretton -Woods zugefallen war. Und das gegenwärtige internationale Finanzsystem ohne eine bestimmende Rolle der US-Zentralbank ist nicht mehr das System, das wir seit 60 Jahren kennen.

Den Finanzmärkten erscheint der Verlust der Marktsteuerungskräfte der US-Zentralbank zur Zeit noch das größere Übel zu sein (9). Nach unserer Auffassung ist jedoch der Verlust ihrer Führungsrolle im Netzwerk der großen Zentralbank das Ereignis, das entscheidend für den im nächsten Jahr zu erwartenden Zusammenbruch sein wird, da das System ohne Steuerung durch eine zentrale Stelle nur schwerlich wird überleben können. Wir rechnen mit dem Zusammenbruch für den Sommer 2008, wenn die Auswirkungen der US-Rezession im Alltag der Menschen spürbar sein und die Zentralbanken Asiens und Europas sich gezwungen sehen werden, rücksichtslos gegen den Führungsanspruch der US-Zentralbank zu opponieren, um die Interessen ihrer eigenen Wirtschaftszonen zu schützen.

In dieser 20. Ausgabe des GEAB vom 15. Dezember 2007 (deutsche Ausgabe 18. Dezember) beschreibt unser Forschungsgruppe detailliert die wachsenden Divergenzen in den Strategien der vier großen Zentralbanken (Federal Reserve USA, Europäische Zentralbank, Bank of England, Schweizer Nationalbank)

Wenn man bedenkt, dass schon heute, wo die Auswirkungen der US-Rezession noch nicht im Alltag der Menschen spürbar sind, solche Spannungen im Netzwerk der großen Zentralbanken und im internationalen Finanzsystem herrschen, kann man sich ausrechnen, welch zerstörerische Kraft sie entwickeln können, wenn die Krise in den Geldbeuteln der Menschen angekommen sein wird. Dann werden die unterschiedlichen Interessen das System unter einen solchen Druck setzen, dass es im Sommer 2008 darunter zusammenbrechen wird.

Dieser Zusammenbruch wird für die großen internationalen Banken katastrophale Folgen haben, insbs. für die unter ihnen, die selbst heute noch nicht begriffen haben, aus welcher Richtung der Wind weht und die daher weiterhin sehr stark in Dollarwerten engagiert sind, obwohl nichts mehr den Absturz des Dollars aufhalten kann. Die Banken, die die Subprime-Krise nicht zur Kenntnis nehmen wollten, konnten den Konkurs (bisher) vermeiden; dies wird den Banken, die nicht verstehen wollen, dass das internationale Finanzsystem am Zusammenbrechen ist, nicht möglich sein (10).

Für die Anleger und Investoren wird dieser Zusammenbruch ebenfalls große Risiken mit sich bringen. Um sich dieser Risiken zu vergegenwärtigen, genügt es, die Erfahrungen in zwei andere Zeitspannen zu betrachten, in denen bestehende Systeme zusammenbrachen, also 1929 (11) und die folgenden Jahre, bzw. 1973 und bis zum Ende der siebziger Jahre. Unserer Forscher gehen davon aus, dass die Folgen des zu erwartenden Zusammenbruchs noch tiefgreifender sein werden; denn damals war die Finanzmärkte ein Teil der Wirtschaft - heute ist ihre Bedeutung um ein Vielfaches höher als die Realwirtschaft. Wir werden uns in dieser Ausgabe in der Rubrik "Empfehlungen" Ratschläge geben, wie man sich gegen diese Auswirkungen schützen kann.

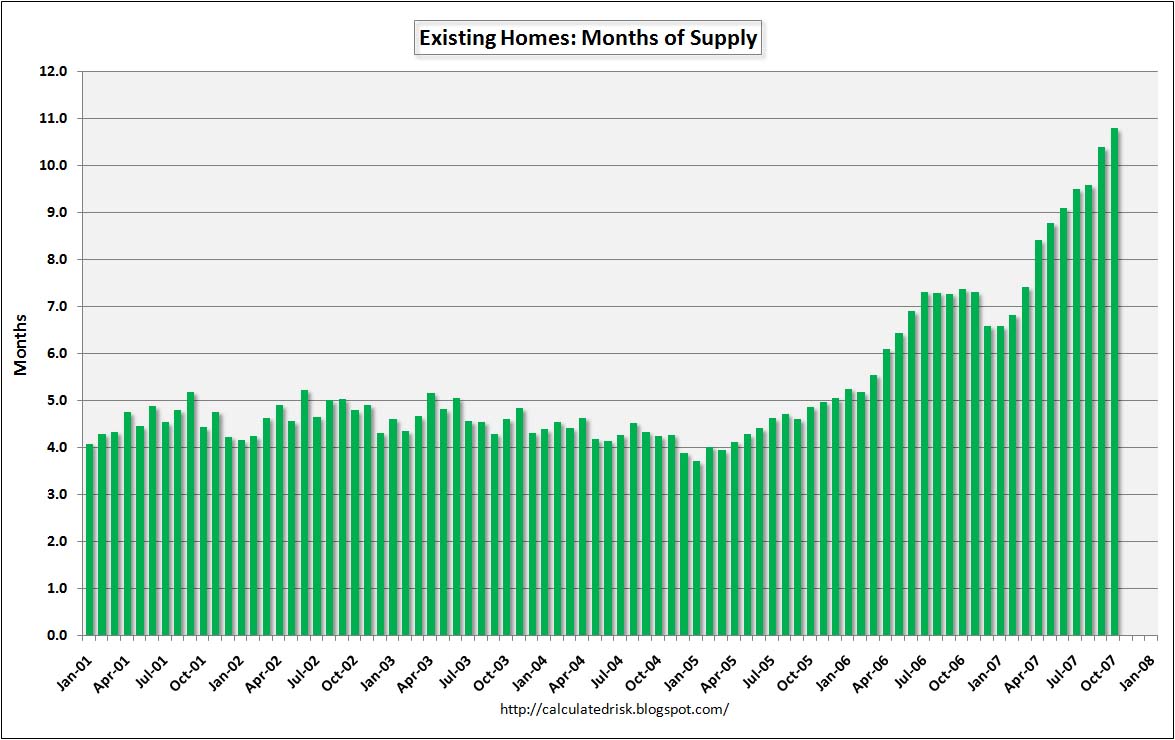

Quartalsmäßige Entwicklung der Privatkredite für die US-Banken (in blau) im Verhältnis zu den privaten Spareinlagen (in rot) - Quelle FDIC - Kommentar: Hier zeigt sich, dass diese beiden Kurven, also ausgegebene Kredite bzw. Einlagen, seit Ende 2006 in bi

Zur Zeit ist es noch zu früh, um vorher zu sagen, wie sich das internationale Finanzsystem nach dem Zusammenbruch neu organisieren wird. Bis zum Sommer 2008 sollte dies jedoch mit relativer Exaktheit möglich sein. Für unsere Forscher ist aber schon heute klar, dass ein solches neues System nur durch eine enge Zusammenarbeit der Asiaten, geführt von dem Tandem China-Japan, der Europäer, also im wesentlichen die Eurozone, der Russen und der erdölfördernden Länder geschaffen werden kann.

Leidtragender dieser Entwicklung werden die USA sein. Denn natürlich wird das neue System nicht mehr vor allem ihrem Nutzen dienen, wie dies die letzten sechzig Jahre der Fall war. Die neue US-Regierung, die ab Januar 2009 im Amt sein wird, wird sich in einer sehr schwierigen Lage finden. Ihre Hauptsorge muss sein, die USA durch diese schwierige Phase des Systemwechsels zu steuern. Dies wird nur unter wirtschaftlich und finanziell schwer zu tragenden Belastungen möglich sein, die zu schultern die Rezession noch erschweren wird. Die Europäer und Asiaten wären gut beraten, dies zu bedenken, um zu verhindern, dass aus den Trümmern des Zusammenbruchs Chaos erwächst.

--------

Noten:

(1) Vgl. hierzu insbs. die 18. Ausgabe des GEAB für die Abfolge der Ereignisse innerhalb der Aufprallphase

(2) Und zwar im Ausgleich für jegliche Art von Sicherheite sowie unter Zusicherung, dass diese Inanspruchnahme nicht publik werde. Ein solches Vorgehen läßt sich eigentlich nur mit Panik erklären und läuft im Endeffekt auf einen Bail-out der Banken mit staatlichen Mitteln hinaus. Für weitere Einzelheiten verweisen wir auf die Webseite der US-Zentralbank (US Federal Reserve).

(3) Mit diesem Trick versucht die US-Zentralbank, Zeit zu gewinnen, denn es bedürfte eines Wunders, damit diese Anlagenwerte wieder den Wert erlangen, der ihnen bis zum Sommer 2007 zugeschrieben war. Da es sich um Kredite der US-Zentralbank an die Banken handelt, sind diese eigentlich verpflichtet, sie im Lauf des Jahres 2008 wieder zurück zu zahlen. Oder sie werden es so machen wie Northern Rock im Vereinigten Königreich, also zusammen brechen und damit mit einem Schlag zweistellige Milliarden-USD-Beträge zu vernichten. Insoweit ist es sehr hilfreich, die Aufstellung der Wertstellungen der Vermögensteile (Discount Collateral Margins Table) zu lesen, die von der Fed als Sicherheiten für Kredite akzeptiert werden. Dabei kann man feststellen, dass die US-Zentralbank 70 bis 80 cent pro Dollar für Vermögenswerte leiht, die heute auf dem Markt noch nicht einmal mit der Hälfte dieser Summe gehandelt werden (vgl. 19. Ausgabe des GEAB)

(4) Quelle: Reuters, 14.12.2007

(5) Quelle: Bloomberg, 13.12.2007

(6) Jenseits der täglichen Verlautbarungen über die notwendigen Rückstellungen für Abdeckung von Verlusten aus der Subprime-Krise oder wegen anderer CDOs gibt die FDIC (Federal Deposit Insurance Corporation, deren Aufgabe darin besteht, die Spareinlagen der bei diesem Bundesversicherungssystem versicherten US-Banken bis zu einer Höhe von 100.000 Dollar zu garantieren) in ihrer Pressemitteilung vom 28. November 2007 bekannt, dass der Netto-Ertrag der US Banken im dritten Quartal 2007 um 28,7 Milliarden zurückgegangen ist.

(7) Vgl die hier wiedergegebene Liste der wichtigsten US-Geschäftsbanken

(8) Vgl. hierzu den sehr interessanten Artikel von Paul Krugman in International Herald Tribune, v. 14.12.2007.

(9) Die Anonymität ermöglicht den Banken, die sich bei der US-Zentralbank Geldmittel besorgen, ohne dass ihre ernsthaften finanziellen Schwierigkeiten bekannt werden. Auf diese Art und Weise versucht die US-Zentralbank zu vermeiden, dass sich in den USA das gleiche ereignet wie in Großbritannien bei den Geldspritzen der Bank of England für Northern Rock.

(10) Hierzu möchten wir bekannt geben, dass Lehman Brothers, eine der beiden großen US-Banken neben Goldman Sachs, die das Subprime-Desasater vermeiden konnten, weil sie ihre Anlagen noch rechtzeitig gegen Ende 2006 abstießen, die einzige große internationale Bank war, die sich mittels eines Leitenden Mitarbeiters ihrer Londoner Niederlassung unmittelbar mit uns im Frühjahr 2006 in Verbindung setzte, um sich über den Hintergrund unserer Analysen zur US-Subprimekrise zu informieren. Denn schon im Februar 2006 sagten wir das Platzen der US-Immobilienblase und ihre finanziellen Auswirkungen voraus, was uns in den traditonellen Bankerkreisen einen hohen Bekanntheitsgrad eingebracht hat. Interessant ist jedoch, dass die meisten anderen großen Banken in den USA und Europa, die uns kontaktiert haben, dies erst im Frühjahr 2007 unternahmen; mit anderen Worten, als es zu spät war, um noch zu reagieren. Diese Anekdote zeigt nach unserer Auffassung, wie wichtig Voraussagen in einem komplexen System sind, wie die Welt, in der wir leben, es ist. Man muss agieren, bevor das Problem sich stellt, denn wenn es sich stellt, ist es im allgemeinen zu spät, um noch etwas zu bewirken. Und in diesem Fall kann man den Unterschied beziffern: 886 Millionen Dollar für Lehman Brothers, im Vergleich zu 49 Milliarden Dollar an Finanzspritzen, die Citigroup für einige seiner Investitionsfonds setzen musste, um sie vor dem Konkurs zu retten.

(11) Hierzu ist die Lektüre des Arbeitsdokuments 197 der Bank für den internationalen Zahlungsverkehr interessant, der den Titel trägt: 130 Jahre Zusammenarbeit zwischen den Zentralbanken aus der Sicht der BiZV, erstellt von Claudio Borio und Gianni Toniolo. Er verschafft eine historisch sehr notwendige Perspektive auf die Turbulenzen, die dem internationalen Finanzsystem bevor stehen.

Mardi 18 Décembre 2007

MfG

Knappschafftskassenvampir