Dies erwartet Marc Chandler. Der Street.com-Autor leitet hauptberuflich einen Hedgefond, der u. a. long Yen (gegen Dollar) ist und daher zu denen zählt, die jetzt auf dem falschen Fuß erwischt wurden (siehe letztes Posting).

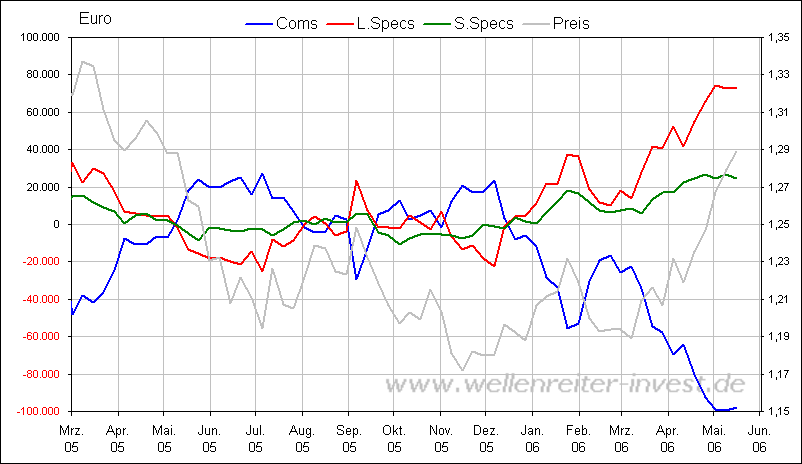

Chandler rechnet damit, dass die Dollar-Erholung der letzten Woche nur ein technische Korrektur war.Wie viele "large Specs" ist Chandler ein "Fundo-Chartist" (das Wort stammt von mir, siehe mein Thread), der bei charttechnischen Bewegungen IM NACHHINEIN fundamentale Erklärungen dafür sucht - und dem Trend folgt. Der COT-Chart - unten die neueste "Ausgabe" - belegt, dass die "Large Specs" mit ihren Trendfolge-Spekulationen am Ende immer falsch liegen. Ihre Positionierung ist kurz vor Wenden stets am größten, d. h. bei EUR/USD 1,30 hatten sie die maximale Zahl an Euro-Long-Positionen. Large specs sind daher ein Kontraindikator (ähnlich wie das Put/Call-Verhältnis). Wie man im aktuellen COT-Chart unten sieht, beginnen die Specs ihre Euro-longs nun langsam zurückzufahren. Der Downtrend bei EUR/USD dürfte sich daher IMO in den nächsten Wochen fortsetzen. Er ist meist erst dann am Ende, wenn die Specs und die Commercials im Chart komplett die Seite getauscht haben (wie z. B. im Juli 2005).

Trotzdem ist interessant, was Chandler zu EUR/USD zu sagen hat. Sein Kursziel bis Jahresende ist 1,33 (ich rechne eher mit 1,20). Bezeichnend ist, dass er vor zwei Monaten, als EUR/USD bei 1,19 stand, die Meinung vertrat, der Dollar sei "fair bewertet". (Damals war er halt noch "Trendfolger nach unten".)

Market Commentary

Inflation Claws Away Fed PauseBy Marc Chandler

Street.com

5/19/2006 8:06 PM EDT

I've warned since last spring that the market has consistently underestimated the magnitude and duration of the Federal Reserve's monetary-tightening cycle. I thought that the Fed would pause in June and resume raising rates after the summer, but a June rate hike seems likely -- I now expect rates to reach at least 5.75% by the end of the year, with upside risks into early next year.

Measured inflation is rising, as are several indicators of inflation expectations. Headline consumer prices are rising at an annualized rate of over 5% so far in 2006, making it the worst start to a year since 1990. The core measure is up 2.3% from year-ago levels. The pace of core CPI hit 2.4% last February; it appears poised to surpass that level this summer, partly due to businesses passing on higher energy prices to the consumer. The Fed's preferred measure, the deflator of core personal-consumption expenditures, rose 2% year over year at the end of the first quarter. The April data will be released May 26 and is expected to rise above the upper end of the implicit target of 2% for the first time since last March. The core measure peaked in November-December at 2.3%; there is a clear risk that this will be surpassed in the coming months.

Other measures of inflation also appear to confirm increased pressure, including surveys like the Philadelphia Fed's prices-paid index for manufacturers, which is at a seven-month high. Import prices surged in April to a 5.9% year-over-year rate after trending lower from almost 10% in September to 4.6% in March. Average hourly earnings in April rose at a 3.8% year-over-year clip, the strongest rise since late 2001.

However, it must be understood that the Fed responds to inflation expectations, not simply recorded inflation. This is more difficult to measure, though going forward, expectations deserve and will likely receive greater attention from market participants. The spread between conventional Treasuries and inflation-protected securities (TIPS) has widened noticeably in recent weeks; early this month we flirted with a 10-year spread of 275 basis points, nearly the widest ever. Of course, this spread reflects three elements: inflation, inflation expectations and a liquidity premium, as the TIPS are not nearly as liquid as conventional Treasuries. In the past, the Fed has cited the University of Michigan's survey as well, but there are a number of shortcomings of such surveys, like lack of availability in real time and methodological issues.

There are other developments that appear consistent with rising inflation fears, including the steepening of the U.S. yield curve and, arguably, the broad-based decline in the dollar's value. The broad trade-weighted measure of the dollar has fallen by about 7% since early March. Such a decline, should it be largely sustained, offsets some of the Fed's tightening. There isn't a hard-and-fast tradeoff, but generally speaking, given the role of the U.S. external sector, the 7% depreciation of the trade-weighted dollar may be tantamount to around a 50-bp cut in rates.

Shades of 1987

Market participants often look for historical parallels. After the recent Group of Seven meeting, the obvious parallel was the Dubai G7 meeting in 2003, which called for greater flexibility for Asian currencies and helped fuel a six-month decline in the dollar. The dollar fell persistently against the yen during that period, even though it marked a period of unprecedented heavy dollar purchases by the Bank of Japan.

However, when considering U.S. monetary policy, a comparison with 1987 may be more revealing. Recall that Alan Greenspan took the helm of the Fed from Paul Volcker, who was retiring from the post. Volcker's reputation as chairman of the Federal Reserve was as a tough inflation fighter. At his first opportunity, Greenspan hiked the federal funds and discount rates, in early September. Germany and Japan, fearful of their own inflation pressures, were threatening to raise rates further. U.S. Treasury Secretary James Baker reportedly threatened to let the dollar fall if Germany and Japan raised rates and/or failed to boost domestic demand. This set the stage for Black Monday (Oct. 19), when global equities melted down and the dollar sank like a brick.

Although Greenspan had Washington experience, in many ways he was an unknown quantity from the investor's perspective, especially given the respect Volcker had earned. The market had to test his mettle, and would do so a number of times during his tenure. Benjamin Bernanke finds himself in a similar position. Although Bernanke was a Fed governor, succeeding Greenspan would be a challenge for anyone, and his mettle is now being tested.

Some pundits have argued that grown men, especially those with Bernanke's credentials, need not prove themselves. I see things differently. In addition to economic analysis, I argued that game theory supported a number of rate hikes early in Bernanke's tenure. I think talk of the Fed losing credibility is probably an exaggeration. A close reading of the record would indicate that Bernanke never indicated that the Fed would pause in June, though it was clear that if the data was sufficiently in line with the Fed's expectations, a pause was desired, if for no other reason than to see the impact of past hikes and to try to gain some strategic flexibility.

The market has repeatedly thought "one and done" when it comes to the Fed this year. Many observers misunderstood Bernanke, not because the chairman misspoke or was purposely ambiguous like his predecessor, but due to preconceived ideas and biases.

The appointment of Federal Reserve Governor Donald Kohn to be vice chairman will help reassure the market. Kohn was reportedly considered for the chairmanship. He has been at the Fed for more than 35 years -- more time than the other governors combined. It is also noteworthy that Kohn is not in favor of a formal inflation target, which Bernanke has advocated. This signals that Bernanke doesn't have to be surrounded by those who agree with him.

Forex Will Cancel Out Fed

I tend to discount the role of external imbalances in explaining or predicting currency moves; my emphasis has been on interest rates, differentials and the slope of the curve. However, I'm afraid that, just as in 1987 and 2003, the G7 and IMF have repoliticized the foreign-exchange market. The additional rate hikes that we expect the Federal Reserve to deliver will, in effect, simply offset the easing impulse generated by the falling dollar.

[Wenn Chandler nach "Zins-Differenzen" geht, sollten nach Lehrmeinung die hohen Zinsen den Dollar eigentlich stützen... - A.L.]

In addition, the European Central Bank is looking more aggressive than I expected.

[Die EZB wird, wie Bretons Äußerungen zeigen, mit steigendem Euro immer "softer" - A.L.]

The Bank of England, which I'd thought could cut rates, now looks poised for a hike. Japan also appears poised to raise rates earlier and more aggressively than we thought...

[stimmt auch nicht mehr, deshalb fiel der Yen ja gestern, siehe letztes Posting - A.L.]

..., likely at the start of the year. I believe the dollar's rise over the past week is a temporary countertrend, one that will provide a new opportunity to raise dollar hedges or reallocate funds away from the U.S.

I have raised my year-end euro forecast to $1.33 and have reduced my dollar forecast to 106 yen.

FAZIT: Chandler scheint die G7- und IWF-"Politik" zu überschätzen. Einen stark abwertenden Dollar will niemand. Wenn Europa mit teurem Euro die Zeche für US-Verschwendungssucht zahlen soll - in Gestalt zurückgehender Exporte - , wird die EZB beizeiten verbal und real intervenieren und durch Zurückhaltung bei weiteren Zinserhöhungen erstens den Euro als Anlagewährung unattraktiver machen und zweitens der durch die Dollarabwertung bedrohten EU-Exportwirtschaft auf die Sprünge helfen.

(Verkleinert auf 69%)