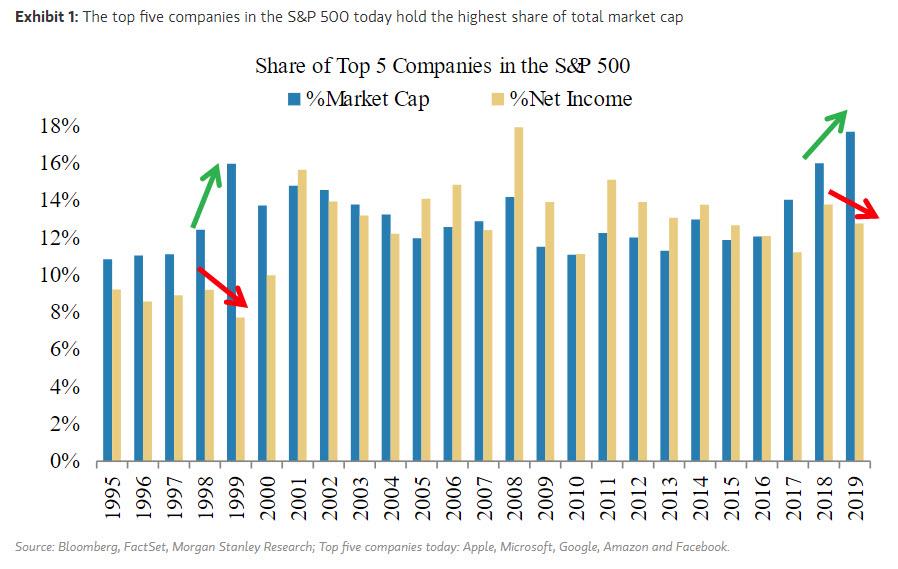

Fünf SP-500-Aktien machen zurzeit 18 % der Marktkapitalisierung des SP-500-Index aus.

Morgan-Stanley Analyst M. Wilson (siehe unten) führt das auf die "außerordentliche Liquidität" zurück, die die Zentralbanken in die Märkte pumpen. Diese Liquidität fließe zugleich in die liquidesten Aktien.

Die Lage sei aktuell ähnlich wie Ende 1999, als die Fed aus Angst vor dem Jahr-2000-Crash (Y2K- bzw. Computer-Crash) die Märkte mit Geld vollpumpte.

Kommentar A.L.: Wir haben also zum wiederholten Mal das Phänomen, dass die Fed die Märkte aus Angst von einem Crash aufbläst. Ende 1999 drohte der Y2K-Crash; im letzten Herbst ist die Liquidität der Märkte von einem Tag zum anderen ausgetrocknet (ähnlich wie im Sommer 2007), und die Overnight-Zinsen schossen auf 10 % hoch. Daraufhin startete die Fed ihr extremes Repo-Stützprogramm, das eine Art "Schatten-QE" darstellt. Damit blies sie die US-Indizes trotz latenter Krise auf ATHs auf.

2008 floss das viele Geld, das die Fed als Reaktion auf den Liquiditätsengpass vom Sommer 2007 (PE-Krise) in die Märkte gepumpt hatte, auch stark in Rohstoffe. Öl stieg im Sommer 2008 bis 150 Dollar. Doch die eigentlich Krise - die damals latent brodelnde Banken/Hypo-Krise - ließ sich mit dieser Inflationierungs-Strategie nur aufschieben. Bereits im März 2008 erfolgte die erste große US-Bankpleite (Bear Stearns musste zwangsübernommen werden), und im Herbst folgte Lehman.

FAZIT: Seit 1999 sehen wir die Fed im Überlebensmodus. Sie pumpt die Märkte von einer Krise zur nächsten. Je mehr Schulden in das Kredit-Kartenhaus fließen, desto windanfälliger wird es. Bislang endeten alle Pumpaktionen der Fed letzlich in einem Fiasko.

----------------------------------

www.zerohedge.com/markets/...ened-between-stocks-and-earnings

Yesterday, when looking at the composition of the ongoing market meltup, Morgan Stanley flagged just how uneven the leadership distribution has become highlighting the "other 1 percent", namely the handful of tech names that have been responsible for the bulk of the S&P's move higher in 2019, and noting "that in a world of low growth, limited pricing power and now rising costs, it’s clear that bigger is better and scale matters." As a result, "currently, the top five companies in the S&P 500 (the other 1 percenters) make up 18% of the total market cap."

As Morgan Stanley's equity strategist, Michael Wilson, writes today "this is the most extreme this metric has ever been, including the tech bubble of the late 1990s..... "this divergence is the result of the extraordinary liquidity being provided by the world’s central banks, which is flowing to the most liquid and largest names in the S&P 500. This also recalls 1999, when the Fed expanded its balance sheet at the end of the year and early in 2000 as a precaution against Y2K disruption."

(Verkleinert auf 62%)

Werbung

Werbung