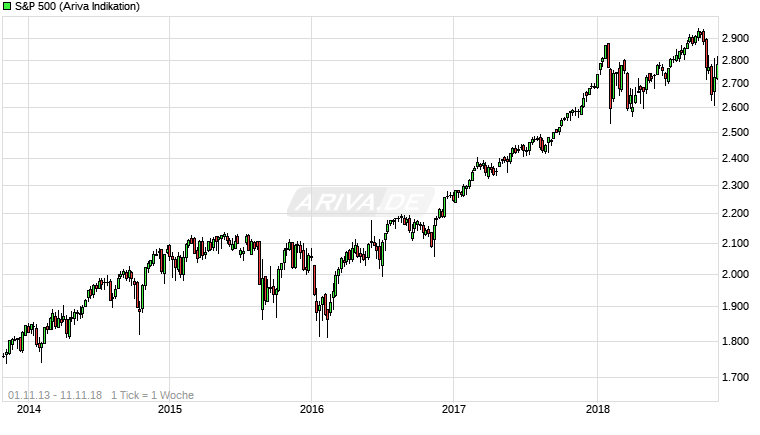

Roberts hält es für wahrscheinlich, dass der 2009 begonnen Bullenmarkt demnächst endet. Näheren Aufschluss darüber soll die Marktentwicklung Anfang 2019 geben. (Ich rechne im Januar mit einem größeren Abverkauf, wie schon mehrfach geschrieben.)

Roberts baut jetzt schon langsam bzw. vorsorglich Long-Positionen ab, um bei einem größeren Rutsch nicht (gemeinsam mit den Lemmingen) panikartig verkaufen zu müssen: "Wenn wir [erst lange] auf Bestätigung warten, könnte [im Rutsch] mehr Kapital verbrannt werden, als uns lieb ist."

www.zerohedge.com/news/2018-11-08/...bull-market-have-shifted

Conclusion:

The tailwinds that existed for the market over the last couple of years from tax cuts, to natural disasters, to support from Central Banks have now all run their course.

The backdrop of the market currently is vastly different than it was during the “taper tantrum” in 2015-2016, or during the corrections following the end of QE1 and QE2. In those previous cases, the Federal Reserve was directly injecting liquidity and managing expectations of long-term accommodative support. Valuations had been through a fairly significant reversion, and expectations had been extinguished.

None of that support exists currently.

There is a reasonably high possibility, the bull market that started in 2009 has ended. However, we will likely not know for certain until we get into 2019, but therein lies the biggest problem. Waiting for verification requires a greater destruction of capital than we are willing to endure.

We have already taken steps to reduce equity risk and will do more on rallies that fail to re-establish the previous bullish trends in the market. If I am right, the more conservative stance will protect capital in the short-term. The reduced volatility allows for a logical approach to further adjustments as the correction becomes more apparent. (The goal is not to be forced into a “panic selling” situation.)