- offenbar eine Folge des stark steigenden Internethandels. Der Boom bei Amazon und Co. beschert traditionellen Shopping-Malls herbe Umsatzeinbrüche und Leerstände.

Wegen der sich häufenden Shop-Pleiten und der Umsatzrückgänge sinken Wiederverkaufs- und Beleihungswert der Malls, während die Finanzierungskredite in voller Höhe stehen bleiben. Die Finanzierung ist meist sehr hoch gehebelt, so dass schon bei relativ geringen Wertrückgängen "negative equity" droht - ähnlich wie nach 2005 bei vielen US-Eigenheimkäufern.

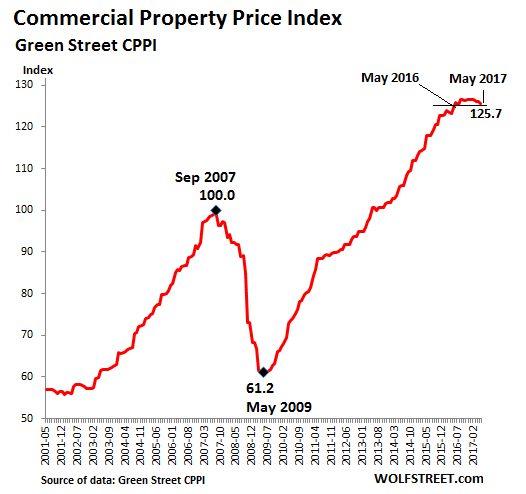

Commercial Real Estate (CRE) ist eine typische Boom-und-Bust-Branche, wie unten schon der Chartabschnitt 2001 bis 2009 (linke Hälfe) zeigt. Aktuell droht aus der letzten, 2009 losgetretenen Boom-Phase die Luft zu entweichen.

Beim Betrachten des CRE-Charts (unten) fällt auf, dass er kaum Vola aufweist und "wie an der Schnur gezogen" verläuft. Dadurch erhält einer Kehrtwende (so wie jetzt nach unten) eine weitaus höhere Prognose-Kraft. Die Topbildung ging über die letzten zwei Jahre, aktuell sind merkliche Rückgänge angesagt. Der Sub-Index für Shopping-Malls fiel im Mai um herbe -2,8 % - und in den letzten drei Monaten um -5 %. Industrie-Immobilien sind derzeit preisstabiler, so dass sich der CRE-Gesamtrückgang (noch) in Grenzen hält.

Der CRE-Sektor ist so groß und operiert so hoch gehebelt, dass die Fed bei einem Absacker wenig auffangen könnte. Probleme bekämen mal wieder die US-Banken und -Versicherungen. Beide haben bei CRE nicht weniger als 2 Billionen (engl. trillion) Dollar im Feuer.

Insgesamt stehen CRE-Kredite in Höhe von 3,5 Billionen aus. Das ist fast so hoch wie die Bilanzsumme der Fed.

wolfstreet.com/2017/06/07/...-so-big-even-the-fed-is-fretting/

Commercial Real Estate’s boom-and-bust cycle heads south

Commercial real estate’s eight-year boom reached such breath-taking levels that even the Fed has been pointing it out as one of the reasons for tightening monetary policy. The Fed is worried because of the size of the sector, its leverage, and what it did to the banks during the Financial Crisis. And now commercial real estate prices are heading south once again....

...One of the primary drivers of the decline are the values of retail malls that have been getting hit by store closings and bankruptcies of their tenants as brick-and-mortar retail is melting down. So the sub-index for malls fell 2.8% in May and 5% for the past three months, and is down year-over-year. Other weak areas are apartment buildings. But industrial space – such as warehousing, one of the beneficiaries of the shift to online retail – remains strong.

Boston Fed President Eric Rosengren, one of the earliest advocates of unwinding QE, started warning about the CRE bubble last year. A couple of months ago, he gave a presentation on what CRE could do to “financial stability,” with some stunning charts.

The “significant decline in collateral values” of both commercial and residential real estate was “the root cause of the financial crisis,” he said. Currently, financial institutions hold $3.8 trillion of CRE loans:

- Banks: $2.02 trillion or 53% of total

- Life insurers: $460 billion or 12% of total

- Government Sponsored Enterprises (such as Fanny Mae) and Agency commercial mortgage-backed securities: $521 billion or 14% of total

- Non-Agency commercial mortgage-backed securities: $544 billion or 14% of total.