Viele US-Firmen sind overleveraged, die Verschuldungsraten sind aufgrund des langanhaltenden Niedrigzinsumfelds mittlerweile wesentlich höher als zu Beginn der Finanzkrise vor 10 Jahren. Da steigende Zinsen und eine rekordhohe Verschuldung schwerlich zusammenpassen, äußert sich zunehmend eine gewichtige Schar von Marktteilnehmern in den USA recht skeptisch bzgl. der künftigen Entwicklung von Unternehmensanleihen. Aktuell zu lesen bei Bloomberg:

"Corporate America Will Bring Next Wave of Pain, Money Managers Warn"

Corporate America will beget the next wave of financial pain, or even recession, a growing choir of the world’s biggest money managers is warning.....

.....Debt levels crept up as central banks suppressed borrowing benchmarks, with the proportion of global highly-leveraged companies -- those with a debt-to-earnings ratio at five times or greater -- hitting 37 percent in 2017 compared with 32 percent in 2007, according to S&P Global Ratings. When that burden collides with rising rates, it could cause a recession in the “late 2019 to mid 2020” window, Minerd wrote in an email.....

Weiter hier

www.bloomberg.com/news/articles/...pain-on-corporate-leverage

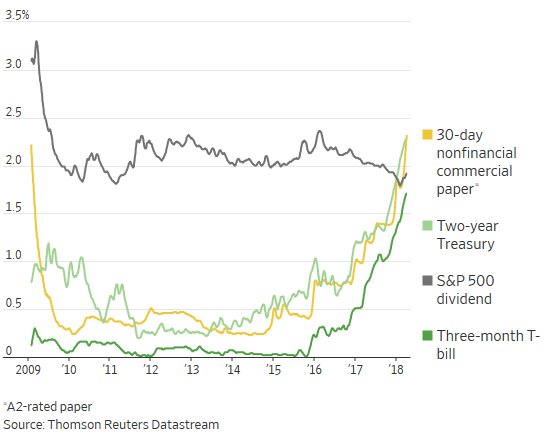

Die Zinsen für kurzfristige Geld-Anlagen in den USA sind in den vergangenen 12 Monaten massiv angestiegen und haben die Dividende des S&P500-Index teilweise bereits deutlich überholt. Aus dem Wall Street Journal dazu:

"Cashing In: Why Cash Should Be in Your Portfolio Again"

As volatility returns to the markets and interest rates rise, cash is turning out to be a safe asset

.....A bank deposit still pays next to nothing, but money-market funds are offering as much as 1.75%. Lend to high-quality companies for 30 days in the commercial paper market, and the yield of 2.4% is above inflation and more than the 1.95% dividend yield from the S&P 500. Locking money up for 10 years in a Treasury bond offers less than 0.5 percentage point more, the smallest premium since just after Lehman collapsed.

Those who want the security of holding government paper have to lock up their money for just a year to beat the dividend yield on stocks, with the 1-year Treasury bill yielding 2%. Again, if you can get 2% for a year, is it worth locking up money for 10 years in a Treasury bond for an extra 0.8 percentage point a year.....

Weiter hier

www.wsj.com/articles/...be-in-your-portfolio-again-1522943904