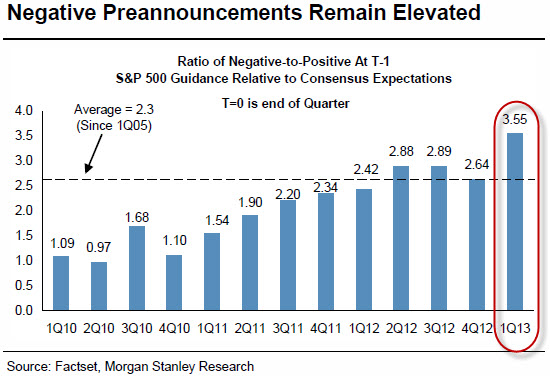

ZH und das WSJ weisen darauf an, dass das Verhältnis von negativen zu positiven Gewinnausblicken auf Rekordhoch steht - bei 3,55. D.h. auf einen positiven Gewinnausblick kommen 3,55 Gewinnwarnungen.

Am Top des letzten Bullenmarktes im Herbst 2007 stand diese Ratio bei nur 2,38.

Weiterhin notierten Aktien, deren Gewinnausblick gesenkt wurde, zwei Tage später im Schnitt nur 0,3 % tiefer, und einige stiegen sogar.

We noted last night the 'six charts' that represent the sum total of the hopefulness of these markets with relation to fundamental earnings but it is the ratio of negative to positive earnings guidance - which stands at a record high - that should worry investors the most (and doesn't). As the WSJ notes, in the last bull market, the negative corporate guidance ratio hit a peak of 2.38 in the third quarter of 2007 - just as that bull market was ending (and troughed at 0.97 right as the bottom was in in stocks in Q1 2009). The current 3.55 ratio is the highest on record.

But what is more representative of the market's absolutely sanguine nature is that just 2 days after guiding earnings down, stock prices are down just 0.3% (and half the stocks actually rose). As the WSJ concludes, and we tend to agree, watch out. There may be a nasty drop on the other side of this wall.

www.zerohedge.com/news/2013-04-02/you-know-markets-euphoric-when

Warum ist das ein Topsignal? Ist es nicht bärisch, wenn Firmen vermehrt Gewinnwarnungen abgeben? Wieso stehen Aktien dann trotzdem auf ATH?

Meine Antworten:

Aktien haben die ATHs nicht zuletzt dank überzogener Gewinnausblicke erreicht. Dabei wurde der Markt u. a. von Hype und Aufwärtsmomentum getrieben. Eigentlich müssten die Aktien nun, da überwiegend Gewinnwarnungen kommen, wieder fallen. Doch solange ein "intakter Uptrend" im Gesamtmarkt besteht, lauern überall

bislang zu kurz gekommene Dip-Buyer (darunter Fonds mit Performanceangst), die noch irgendwo halbwegs günstig einsteigen wollen. Bullenmärkte sind deshalb "sticky". D.h. Aktien, die zuvor gestiegen waren, fallen selbst dann nicht, wenn ihre Zahlen unter Erwartung liegen.

In einem etablierten Down-Trend sieht die Sache komplett anders aus: Die gleichen Gewinnwarnungen würden dann für starke starke Kursverluste (-5 bis -10 %) in den betroffenen Aktien sorgen. Denn dann gibt es kaum noch Dipbuyer (Antizykliker sind eher selten...), sondern überwiegende genervte Longs, die "bestens" raus wollen, und shortende Hedgefonds, die daran verdienen, weiter auf die Kurse zu drücken.

Werbung

Werbung

{kind=link}