da die vorhandenen threads alle etwas älter sind, eröffne ich einen neuen

... hier könnte durchaus was drin sein, denn...

EnCana Corporation is North America's largest natural gas producer, with more than 80 percent of its production being natural gas. The company produced 1.4 trillion cubic feet of natural gas in 2008 - enough to heat nearly 11 million homes for one year.

--------------------------------------------------

When you see a headline "EnCana (ECA) cited as next possible takeover target after $29 billion XTO acquisition (XTO)," it's bound to raise some eyebrows. After all, we're talking about North America's biggest natural gas producer here, and Canada's biggest energy company up until it spun off its oil assets a couple of weeks ago.

So, when the Canadian Press ran that exact headline on a story Tuesday afternoon, I figured I should check it out. Was Philip Skolnick, Genuity Capital's energy analyst in Calgary, actually saying - as the CP headline suggests - that he thinks that after Exxon Mobil's (XOM) big takeover of U.S. natural-gas heavyweight XTO Energy earlier this week, EnCana might be in the crosshairs of some other big oil multinational looking to grab some high-potential shale gas assets?

"No, I don't want to say they're a target," Mr. Skolnick clarified in a telephone interview. "But that's where people are going to put their money."

There's a certain logic to it. If big oil companies are buying up big North American natural gas players, there's no one bigger than EnCana. If they're looking at Canada, it's the natural starting point, and the first company that comes to mind for investors.

Plus, EnCana has just made itself more attractive as a takeover target - first, because it's roughly half the size it used to be as a result of the spin-off of Cenovus Energy Inc. (CVE) (the company's former oil assets), and second, because it's now a pure natural gas play. No need for a buyer looking for a foothold in the natural gas market to get stuck with a bunch of annoying non-gas assets that it would likely want to divest.

As of Tuesday afternoon, EnCana's market capitalization stood at about $24 billion; add a bit of a takeover premium, and it's clearly in the same ballpark as XTO. If one could be taken over, why not the other, right?

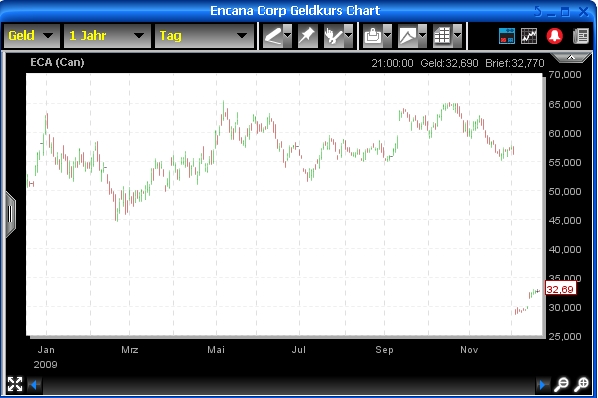

There's a certain simplistic elegance to the argument, and it may have won over more than a few investors: EnCana's stock is up 8% since the Exxon/XTO story broke.

Sure, it may be little more than fantasy; there aren't a lot of companies out there willing to bite off a $25- to $30-billion acquisition, and there's not much evidence that anyone is actively shopping for one. (Indeed, Exxon's purchase of XTO came out of left field for most analysts.)

Still, it's not so far-fetched; it wouldn't be the first time that a big takeover in a sector triggered a round of massive M&As as competitors jockeyed for position. And anyway, can't investors dream a little once in a while? Stocks have gone up on a lot less.

... hier könnte durchaus was drin sein, denn...

EnCana Corporation is North America's largest natural gas producer, with more than 80 percent of its production being natural gas. The company produced 1.4 trillion cubic feet of natural gas in 2008 - enough to heat nearly 11 million homes for one year.

--------------------------------------------------

When you see a headline "EnCana (ECA) cited as next possible takeover target after $29 billion XTO acquisition (XTO)," it's bound to raise some eyebrows. After all, we're talking about North America's biggest natural gas producer here, and Canada's biggest energy company up until it spun off its oil assets a couple of weeks ago.

So, when the Canadian Press ran that exact headline on a story Tuesday afternoon, I figured I should check it out. Was Philip Skolnick, Genuity Capital's energy analyst in Calgary, actually saying - as the CP headline suggests - that he thinks that after Exxon Mobil's (XOM) big takeover of U.S. natural-gas heavyweight XTO Energy earlier this week, EnCana might be in the crosshairs of some other big oil multinational looking to grab some high-potential shale gas assets?

"No, I don't want to say they're a target," Mr. Skolnick clarified in a telephone interview. "But that's where people are going to put their money."

There's a certain logic to it. If big oil companies are buying up big North American natural gas players, there's no one bigger than EnCana. If they're looking at Canada, it's the natural starting point, and the first company that comes to mind for investors.

Plus, EnCana has just made itself more attractive as a takeover target - first, because it's roughly half the size it used to be as a result of the spin-off of Cenovus Energy Inc. (CVE) (the company's former oil assets), and second, because it's now a pure natural gas play. No need for a buyer looking for a foothold in the natural gas market to get stuck with a bunch of annoying non-gas assets that it would likely want to divest.

As of Tuesday afternoon, EnCana's market capitalization stood at about $24 billion; add a bit of a takeover premium, and it's clearly in the same ballpark as XTO. If one could be taken over, why not the other, right?

There's a certain simplistic elegance to the argument, and it may have won over more than a few investors: EnCana's stock is up 8% since the Exxon/XTO story broke.

Sure, it may be little more than fantasy; there aren't a lot of companies out there willing to bite off a $25- to $30-billion acquisition, and there's not much evidence that anyone is actively shopping for one. (Indeed, Exxon's purchase of XTO came out of left field for most analysts.)

Still, it's not so far-fetched; it wouldn't be the first time that a big takeover in a sector triggered a round of massive M&As as competitors jockeyed for position. And anyway, can't investors dream a little once in a while? Stocks have gone up on a lot less.

(Verkleinert auf 93%)

Ich wage mal eine Prognose: Es könnte so oder so ausgehen