San Bernardino, Calif., is slated to become the third California city to file for bankruptcy this summer after City Council members discovered the city had only $150,000 left in its bank accounts.

More Chapter 9 filings could be on the way, with other localities reportedly on the brink of insolvency.

This week, the spotlight shifted to Fresno, Calif. Moody’s Investors Service downgraded the city's issuer rating to the fourth-lowest investment grade, citing its "exceedingly weak financial position" and its difficultly to achieve labor concessions. The rating, which Moody's may downgrade further, affects debt totaling approximately $462 million.

Last week, officials in Compton, Calif., also floated the possibility of bankruptcy. While Compton -- unlike others -- is not hampered by pension obligations, cash flow problems have plagued the city. City Manager Harold Duffey attempted to alleviate fears of bankruptcy on Tuesday, asserting that the city's projected revenues met its annual obligations.

But the vast majority of Chapter 9 filings thus far aren't high profile cases stemming from cities' financial troubles.

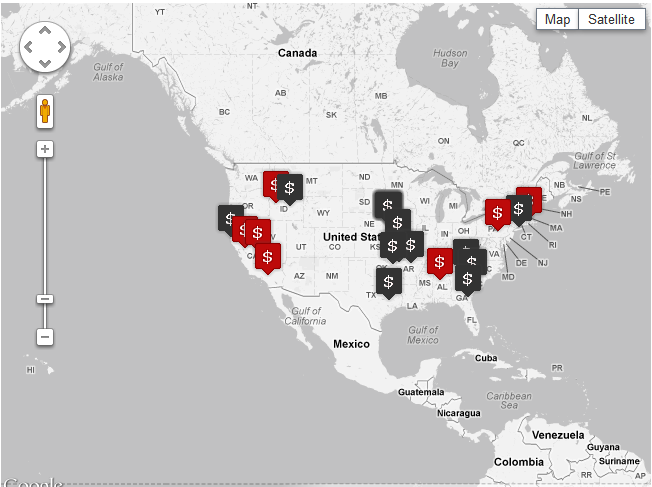

A total of 26 municipalities have filed for Chapter 9 bankruptcy protection since 2010, according to federal records. All but six of these were filed by lesser-known taxing entities, such as local utility authorities, hospitals and other special districts.

In Omaha, Neb., eight Sanitary and Improvement Districts have filed for bankruptcy in recent years.

The Suffolk (N.Y.) Regional Off-Track Betting Corporation filed for bankruptcy in May after the state Legislature changed the state's laws to allow the agency to do so. Suffolk OTB, which manages six branches, reported a $5.1 million net operating loss for 2011.

http://www.governing.com/blogs/by-the-numbers/...ankruptcies-map.html

Karte der bankrotten Städte:http://www.ritholtz.com/blog/wp-content/uploads/2012/07/erwr.png

More Chapter 9 filings could be on the way, with other localities reportedly on the brink of insolvency.

This week, the spotlight shifted to Fresno, Calif. Moody’s Investors Service downgraded the city's issuer rating to the fourth-lowest investment grade, citing its "exceedingly weak financial position" and its difficultly to achieve labor concessions. The rating, which Moody's may downgrade further, affects debt totaling approximately $462 million.

Last week, officials in Compton, Calif., also floated the possibility of bankruptcy. While Compton -- unlike others -- is not hampered by pension obligations, cash flow problems have plagued the city. City Manager Harold Duffey attempted to alleviate fears of bankruptcy on Tuesday, asserting that the city's projected revenues met its annual obligations.

But the vast majority of Chapter 9 filings thus far aren't high profile cases stemming from cities' financial troubles.

A total of 26 municipalities have filed for Chapter 9 bankruptcy protection since 2010, according to federal records. All but six of these were filed by lesser-known taxing entities, such as local utility authorities, hospitals and other special districts.

In Omaha, Neb., eight Sanitary and Improvement Districts have filed for bankruptcy in recent years.

The Suffolk (N.Y.) Regional Off-Track Betting Corporation filed for bankruptcy in May after the state Legislature changed the state's laws to allow the agency to do so. Suffolk OTB, which manages six branches, reported a $5.1 million net operating loss for 2011.

http://www.governing.com/blogs/by-the-numbers/...ankruptcies-map.html

Karte der bankrotten Städte:http://www.ritholtz.com/blog/wp-content/uploads/2012/07/erwr.png

{kind=link}