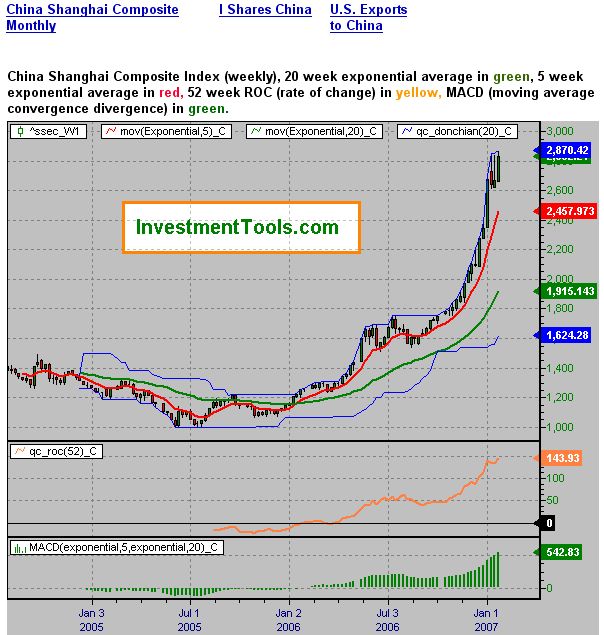

In China herrscht die totale Aktien-Euphorie. Der Shanghai Composite Index (Chart unten) ist parabolisch angestiegen. Investoren verkaufen Haus und Hof, um "dabei" zu sein. Wie sowas typischerweise ausgeht, zeigt der zweite Artikel unten aus Saudi-Arabien, wo die Börsen einen ähnlichen Höhenflug 2006 mit über 50 % Minus beendeten.

China ist aber ein weit wichtigerer Markt. Richard Russell befürchtet im ersten Artikel unten, dass ein China-Crash die ganze (Börsen-)Welt in Mitleidenschaft zieht.

The world according to Richard Russell

U.S., Shanghai stock markets worry veteran gold bug

By Peter Brimelow, MarketWatch

Last Update: 12:01 AM ET Feb 1, 2007

SAN FRANCISCO (MarketWatch) -- Stocks at new highs, but gold gaps up, too.

...

This is one reason why I like Russell: his restless mind.

In Wednesday night's hotline, he went on: "China is in a stock-buying super-frenzy with people mortgaging their homes, taking out loans, doing anything and everything to get in on that wild ride on the Shanghai Exchange. From below 1,000 in June of 2005, the Shanghai Composite has tripled to a current 3,000. The Composite has gone parabolic ... The price of the composite is an astounding 36% above its 40-week moving average.

"If you're looking for international trouble, you might start looking here. The Shanghai Exchange is on fire, and it's hard to know what to expect next. What would a stock crash in China mean? It would have worldwide implications, and it would be deflationary, particularly for commodities. By the way, the Chinese authorities are now actively warning the populace about over-speculating ("irrational exuberance"?)"

I've long been (irrationally?) uneasy about China. See Sept. 1, 2005 column

So this intrigues me.

Ein ähnliche Aktien-Euphorie in Saudi-Arabien endete 2006 mit über 50 % Verlusten. Auch dort hatten Kleinaktionäre Haus und Hof verkauft, um an den "sensationellen Gewinnen" teilzuhaben. Viele von ihnen, darunter viele Frauen, sind jetzt wegen Depressionen in psychologischer Behandlung, sofern sie sich das überhaupt noch leisten können.

Hier die Bilanz des Saudi-Hypes:

YEALD, 30.11.2006 19:13

Saudi-Arabien: Albtraum aus 1001er Nacht

JOURNALISTEN Der Crash an den arabischen Börsen traf besonders Saudi-Arabien ins Mark. Viele Anleger aus dem wüsten- und ölreichen Königreich verloren über Nacht nicht nur Hab und Gut, sondern offenbar auch fast den Verstand. Ärzte sprechen von einem Massenphänomen.

von Ronald Tietjen

Im islamisch-konservativen Königreich Saudi-Arabien muss man schon sehr verzweifelt sein, um auf offener Straße einen Striptease hinzulegen. Doch selbst davor schrecken frustrierte Kleinanleger derzeit nicht mehr zurück. In Damman ließ ein Kleinanleger laut „Arab News“ seiner Wut freien Lauf und riss sich vor einer Bank buchstäblich die Kleider vom Leib. Dabei schrie er seinen ganzen Frust über hohe Verluste an der Börse heraus. Sein Geld brachte ihm die Aktion nicht wieder, dafür 50 Schläge auf den Allerwertesten.

Der Schmerz der 50 Hiebe wird vermutlich schnell vergehen. Die seelische Pein über den Kursrutsch an der Börse dagegen eher nicht. Doch damit steht der Mann nicht allein da. Laut der Zeitung „Al-Watan“ hat der Börsen-Crash in Saudi-Arabien viele Tausend Anleger so schwer getroffen, dass sie wegen Depressionen und anderer psychischer Leiden arbeitsunfähig sind. In den vergangenen neun Monaten hätten die Ärzte im Königreich allein rund 40.000 Patienten untersucht, die ihre Beschwerden mit hohen Verlusten an der Börse begründet hätten, heißt es in dem Bericht.

>> Hohe Verschuldung

Zu den Betroffenen zählten in überraschend großer Zahl auch Frauen. Viele hätten - ohne Wissen ihrer Männer - zum Teil Häuser und all ihren Schmuck verkauft, um Aktien zu kaufen. Die nach dem Aktiensturz geschockten Gatten haben dann die Scheidung eingereicht, weshalb die Frauen nun in völlig hysterischem Zustand die Ärzte aufsuchten, wird eine Medizinerin zitiert. Lehrer wurden entlassen, weil sie in der Schule online an der Börse handelten statt zu unterrichten. Polizisten erschienen nicht zum Dienst, weil der Kauf von Wertpapieren eine Zeitlang am Tag mehr einbrachte, als eine Woche auf Verbrecherjagd zu gehen.

Gier beherrschte auch lange Zeit die Märkte in Dubai, in Kairo, Doha, Kuwait, Amman und Abu Dhabi. Allein die Verluste des laufenden Jahres belaufen sich nach Angaben von Fondsmanagern inzwischen auf 500 Milliarden Dollar. Von den gigantischen Gewinnen, die seit Anfang 2005 an den arabischen Börsen gemacht wurden, ist fast nichts mehr übrig. Der saudische Tadawul All Share Index hat sich seit Neujahr halbiert. Der Dubai Financial Market Index fiel sogar noch stärker.

>> Verluste lange unbekannt

„Viele arabische Anleger kannten bisher überhaupt keine fallenden Aktienkurse“, so der Londoner Nahost-Börsenexperte Ben Kapetzky zu den Gründen des Hypes. „Die haben niemals erlebt, was es heißt, Geld zu verlieren, weil sie vor noch nicht allzu langer Zeit eingestiegen sind.“ Tatsächlich erlebten die Börsen Arabiens in den vergangenen zweieinhalb Jahren eine Blasenbildung, die zu vergleichen ist mit dem absurden Treiben, was Ende der 90er-Jahre in Deutschland am Neuen Markt ablief. Noch vor drei Jahren besaß nur jeder dreizehnte Saudi Aktien, heute ist es jeder sechste. Psychologen verweisen auf gesellschaftliche Zwänge in dem streng islamischen Land: „Saudis sind Spieler, die aber nicht spielen dürfen. Wetten ist verboten, Automatenspiele auch. Eben alles, was Spaß macht. Das Spekulieren ist so etwas wie ein Surrogat gewesen.“

>> Einstürzende Neubauten

Dass es irgendwann zu einer Konsolidierung oder sogar zu einem Kursabsturz kommen würde, darüber wurde allerdings schon Monate vor dem Crash gefachsimpelt. Auch schon, als in Euro noch Zertifikate aufgelegt wurden, die fantastische Gewinne versprachen. Bereits im März berichtete YEALD über das schlechte Timing des gerade aufgelegten "Dubai Top Select Zertifikat" (ISIN: DE000DB52810) der Deutschen Bank. Das Open End-Papier bildet keinen Index ab, sondern ist als Aktienkorb zu verstehen, der aus nur sieben Aktiengesellschaften besteht, die allesamt vom enormen Immobilienboom in den Vereinigten Arabischen Emiraten profitieren sollten.

Namentlich sind es National Central Cooling Company (TABREED), SHUAA Capital, Union Properties, Dubai Investment, Arab Technical Construction, Amlak Finance und auch Emaar Properties, die für das gigantische Vorzeigeprojekt "Burj Al Arab" verantwortlich zeichnen.

§

Bereits nach wenigen Wochen mussten sich Anleger, die den märchenhaften Prospektunterlagen aufgesessen waren, über ein drastisches Minus ärgern. Die Bilanz ist bis dato nicht besser geworden: der Kursabschlag für 2006 beträgt 51 Prozent. Tendenz: eher weiter sinkend.

Von vielen Fondsmanagern heißt es: Die Börsen Arabiens sind heißer als der Sand der Sahara um die Mittagszeit. Da kann man sich schnell die Finger verbrennen. Privatanleger sollten eher nach Asien oder Südamerika schauen, wenn sie in Schwellenmärkte investieren wollen.

>> Interventionen bisher erfolglos

Viele noch investierte Anleger hoffen auf weitere Interventionen des saudischen Königshauses, das mehrfach bereits an den Börsen aktiv wurde und Stützungskäufe tätigte. Das konnte den Kurssturz bisher nicht bremsen, auch wenn sich die Situation an den Märkten Arabiens wieder leicht zu beruhigen scheint. Die Risikofaktoren sind aber immer noch da: Die Iran-Krise, der brüchige Friede zwischen Juden und Palästinensern, die Unsicherheit über den Ölpreis – in Saudi-Arabien ein Dauerthema auch an der Börse. Viele befürchten größere Abschläge, was vor allem Investoren zu noch mehr Zurückhaltung in die Länder des Nahen Ostens veranlassen könnte. Trotz des rund 25-prozentigen Preisrückgangs seit dem Sommer hält z. B. der Mineralölkonzern ExxonMobil den derzeitigen Ölpreis immer noch für viel zu hoch. "Etwa die Hälfte des Preises ist Spekulation und spiegelt keine Knappheit von Öl wider", sagte Gernot Kalkoffen, Deutschland-Chef von ExxonMobil.

Wenigstens aber sollen jetzt die Benzinpreise sinken in Saudi-Arabien. Von 18 Cents auf 14 Cents pro Liter. Nicht unclever von König Abdallah. Denn wenn der Saudi etwas noch lieber mögen soll als das Zocken an der Börse, ist es Autofahren...

China ist aber ein weit wichtigerer Markt. Richard Russell befürchtet im ersten Artikel unten, dass ein China-Crash die ganze (Börsen-)Welt in Mitleidenschaft zieht.

The world according to Richard Russell

U.S., Shanghai stock markets worry veteran gold bug

By Peter Brimelow, MarketWatch

Last Update: 12:01 AM ET Feb 1, 2007

SAN FRANCISCO (MarketWatch) -- Stocks at new highs, but gold gaps up, too.

...

This is one reason why I like Russell: his restless mind.

In Wednesday night's hotline, he went on: "China is in a stock-buying super-frenzy with people mortgaging their homes, taking out loans, doing anything and everything to get in on that wild ride on the Shanghai Exchange. From below 1,000 in June of 2005, the Shanghai Composite has tripled to a current 3,000. The Composite has gone parabolic ... The price of the composite is an astounding 36% above its 40-week moving average.

"If you're looking for international trouble, you might start looking here. The Shanghai Exchange is on fire, and it's hard to know what to expect next. What would a stock crash in China mean? It would have worldwide implications, and it would be deflationary, particularly for commodities. By the way, the Chinese authorities are now actively warning the populace about over-speculating ("irrational exuberance"?)"

I've long been (irrationally?) uneasy about China. See Sept. 1, 2005 column

So this intrigues me.

Ein ähnliche Aktien-Euphorie in Saudi-Arabien endete 2006 mit über 50 % Verlusten. Auch dort hatten Kleinaktionäre Haus und Hof verkauft, um an den "sensationellen Gewinnen" teilzuhaben. Viele von ihnen, darunter viele Frauen, sind jetzt wegen Depressionen in psychologischer Behandlung, sofern sie sich das überhaupt noch leisten können.

Hier die Bilanz des Saudi-Hypes:

YEALD, 30.11.2006 19:13

Saudi-Arabien: Albtraum aus 1001er Nacht

JOURNALISTEN Der Crash an den arabischen Börsen traf besonders Saudi-Arabien ins Mark. Viele Anleger aus dem wüsten- und ölreichen Königreich verloren über Nacht nicht nur Hab und Gut, sondern offenbar auch fast den Verstand. Ärzte sprechen von einem Massenphänomen.

von Ronald Tietjen

Im islamisch-konservativen Königreich Saudi-Arabien muss man schon sehr verzweifelt sein, um auf offener Straße einen Striptease hinzulegen. Doch selbst davor schrecken frustrierte Kleinanleger derzeit nicht mehr zurück. In Damman ließ ein Kleinanleger laut „Arab News“ seiner Wut freien Lauf und riss sich vor einer Bank buchstäblich die Kleider vom Leib. Dabei schrie er seinen ganzen Frust über hohe Verluste an der Börse heraus. Sein Geld brachte ihm die Aktion nicht wieder, dafür 50 Schläge auf den Allerwertesten.

Der Schmerz der 50 Hiebe wird vermutlich schnell vergehen. Die seelische Pein über den Kursrutsch an der Börse dagegen eher nicht. Doch damit steht der Mann nicht allein da. Laut der Zeitung „Al-Watan“ hat der Börsen-Crash in Saudi-Arabien viele Tausend Anleger so schwer getroffen, dass sie wegen Depressionen und anderer psychischer Leiden arbeitsunfähig sind. In den vergangenen neun Monaten hätten die Ärzte im Königreich allein rund 40.000 Patienten untersucht, die ihre Beschwerden mit hohen Verlusten an der Börse begründet hätten, heißt es in dem Bericht.

>> Hohe Verschuldung

Zu den Betroffenen zählten in überraschend großer Zahl auch Frauen. Viele hätten - ohne Wissen ihrer Männer - zum Teil Häuser und all ihren Schmuck verkauft, um Aktien zu kaufen. Die nach dem Aktiensturz geschockten Gatten haben dann die Scheidung eingereicht, weshalb die Frauen nun in völlig hysterischem Zustand die Ärzte aufsuchten, wird eine Medizinerin zitiert. Lehrer wurden entlassen, weil sie in der Schule online an der Börse handelten statt zu unterrichten. Polizisten erschienen nicht zum Dienst, weil der Kauf von Wertpapieren eine Zeitlang am Tag mehr einbrachte, als eine Woche auf Verbrecherjagd zu gehen.

Gier beherrschte auch lange Zeit die Märkte in Dubai, in Kairo, Doha, Kuwait, Amman und Abu Dhabi. Allein die Verluste des laufenden Jahres belaufen sich nach Angaben von Fondsmanagern inzwischen auf 500 Milliarden Dollar. Von den gigantischen Gewinnen, die seit Anfang 2005 an den arabischen Börsen gemacht wurden, ist fast nichts mehr übrig. Der saudische Tadawul All Share Index hat sich seit Neujahr halbiert. Der Dubai Financial Market Index fiel sogar noch stärker.

>> Verluste lange unbekannt

„Viele arabische Anleger kannten bisher überhaupt keine fallenden Aktienkurse“, so der Londoner Nahost-Börsenexperte Ben Kapetzky zu den Gründen des Hypes. „Die haben niemals erlebt, was es heißt, Geld zu verlieren, weil sie vor noch nicht allzu langer Zeit eingestiegen sind.“ Tatsächlich erlebten die Börsen Arabiens in den vergangenen zweieinhalb Jahren eine Blasenbildung, die zu vergleichen ist mit dem absurden Treiben, was Ende der 90er-Jahre in Deutschland am Neuen Markt ablief. Noch vor drei Jahren besaß nur jeder dreizehnte Saudi Aktien, heute ist es jeder sechste. Psychologen verweisen auf gesellschaftliche Zwänge in dem streng islamischen Land: „Saudis sind Spieler, die aber nicht spielen dürfen. Wetten ist verboten, Automatenspiele auch. Eben alles, was Spaß macht. Das Spekulieren ist so etwas wie ein Surrogat gewesen.“

>> Einstürzende Neubauten

Dass es irgendwann zu einer Konsolidierung oder sogar zu einem Kursabsturz kommen würde, darüber wurde allerdings schon Monate vor dem Crash gefachsimpelt. Auch schon, als in Euro noch Zertifikate aufgelegt wurden, die fantastische Gewinne versprachen. Bereits im März berichtete YEALD über das schlechte Timing des gerade aufgelegten "Dubai Top Select Zertifikat" (ISIN: DE000DB52810) der Deutschen Bank. Das Open End-Papier bildet keinen Index ab, sondern ist als Aktienkorb zu verstehen, der aus nur sieben Aktiengesellschaften besteht, die allesamt vom enormen Immobilienboom in den Vereinigten Arabischen Emiraten profitieren sollten.

Namentlich sind es National Central Cooling Company (TABREED), SHUAA Capital, Union Properties, Dubai Investment, Arab Technical Construction, Amlak Finance und auch Emaar Properties, die für das gigantische Vorzeigeprojekt "Burj Al Arab" verantwortlich zeichnen.

§

Bereits nach wenigen Wochen mussten sich Anleger, die den märchenhaften Prospektunterlagen aufgesessen waren, über ein drastisches Minus ärgern. Die Bilanz ist bis dato nicht besser geworden: der Kursabschlag für 2006 beträgt 51 Prozent. Tendenz: eher weiter sinkend.

Von vielen Fondsmanagern heißt es: Die Börsen Arabiens sind heißer als der Sand der Sahara um die Mittagszeit. Da kann man sich schnell die Finger verbrennen. Privatanleger sollten eher nach Asien oder Südamerika schauen, wenn sie in Schwellenmärkte investieren wollen.

>> Interventionen bisher erfolglos

Viele noch investierte Anleger hoffen auf weitere Interventionen des saudischen Königshauses, das mehrfach bereits an den Börsen aktiv wurde und Stützungskäufe tätigte. Das konnte den Kurssturz bisher nicht bremsen, auch wenn sich die Situation an den Märkten Arabiens wieder leicht zu beruhigen scheint. Die Risikofaktoren sind aber immer noch da: Die Iran-Krise, der brüchige Friede zwischen Juden und Palästinensern, die Unsicherheit über den Ölpreis – in Saudi-Arabien ein Dauerthema auch an der Börse. Viele befürchten größere Abschläge, was vor allem Investoren zu noch mehr Zurückhaltung in die Länder des Nahen Ostens veranlassen könnte. Trotz des rund 25-prozentigen Preisrückgangs seit dem Sommer hält z. B. der Mineralölkonzern ExxonMobil den derzeitigen Ölpreis immer noch für viel zu hoch. "Etwa die Hälfte des Preises ist Spekulation und spiegelt keine Knappheit von Öl wider", sagte Gernot Kalkoffen, Deutschland-Chef von ExxonMobil.

Wenigstens aber sollen jetzt die Benzinpreise sinken in Saudi-Arabien. Von 18 Cents auf 14 Cents pro Liter. Nicht unclever von König Abdallah. Denn wenn der Saudi etwas noch lieber mögen soll als das Zocken an der Börse, ist es Autofahren...

(Verkleinert auf 92%)