Werbung

Werbung

hier die mögliche zukünftige charttechnische Entwicklung eines "Marionetten-Index" wie den DAX zu betrachten, ohne die US-Indizes, welche weltweit den Takt vorgeben, miteinzubeziehen.

Von daher hier nochmals kurz der Blick auf die zyklisch adjustierten Gewinnerwartungen des S&P500 sowie die POMO-Aktivitäten der Fed.

Wie hier im Thread bereits mehrfach vorgestellt, hat der amerikanische Ökonom Robert Shiller eine Kennzahl entwickelt, die die Kurse nicht mit den aktuellen oder für die Zukunft erwarteten Gewinnen vergleicht, sondern mit jenen, die im Durchschnitt der vergangenen zehn Jahre erzielt wurden. Betrachtet man die Entwicklung dieser CAPE (Cyclically Adjusted Price Earnings Ratio) genannten Kennzahl, so liegt sie bezogen auf die Werte des S&P-500-Index bei knapp 24. Damit ist dieser Markt gemessen am langfristigen Durchschnitt von 16,35 (berechnet ab dem Jahr 1881) zum jetzigen Zeitpunkt bereits deutlich überbewertet.

Was aber nun nicht bedeuten soll, dass dieser Trend durchaus noch exzessiv ausgereizt werden kann, wir sahen dergleichen im Jahr 2000, als man den Anlegern weis machen wollte, dass herkömmliche Bewertungsmaßstäbe nicht mehr zählten. Das Ergebnis ist allseits bekannt.

Desweiteren habe ich einen interessanten Artikel von Chris Martenson mitgebracht, in welchem er sich fragt, wie lange die Party an den Börsen noch weiter laufen könnte. Selbstverständlich kann auch Chris Martenson diese Frage nicht beantworten, nur weist Martenson bei der Durchleuchtung der aktuellen Situation schon darauf hin, dass die Fed den Markt recht wohlwollend pusht. Hier ein Ausschnitt des Martensonschen Statements bzgl. der auch schon von mir früher hier im Thread angerissenen marktstützenden POMO-Aktivitäten der FED:

"As an aside, I used to track the Fed's thin-air money programs very closely, and if you had told me as recently as three years ago that the Fed would have been running 11-figure POMO operations each and every month, I would have told you it was unthinkably impossible. But here we are, that is exactly what is happening, and I am largely numb to the process, which worries me somewhat, as it means that my baseline has shifted.

At any rate, the point here is that from those August lows to now, retail investors have taken out far more money from the stock market than they've placed back in; a total of around minus $38 billion.

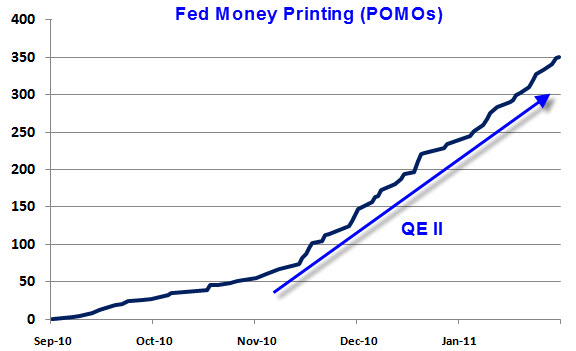

But over that same period, the Fed has placed nearly an entire order-of-magnitude more thin-air money, some $350 billion dollars, into the hands of financial institutions, some of whom consider the stock market their personal playground.

Here's a chart of the cumulative POMOs by the Fed from the end of August 2010 to now.

Should we consider the injection of more than a third of a trillion dollars and a stock market that is up by 20% to be a coincidence? No, not in the least. The stock market has become, if anything, a liquidity gauge first and a discounting machine second. The fundamental that matters most is how much money is flowing into the machine.

So it is my view that the trillions of dollars of thin-air money and deficit spending are finally finding their mark (asset prices) and doing their work, just as I predicted they would. Where some called for deflation to be the irresistible force that would drag us all down, I've consistently leaned towards the side of inflation…..

….The old saying is, Don't fight the Fed. That's good advice. I have dutifully been following the developing story by watching what the Fed does, not what it says, and by letting prices tell me which way the wind is blowing. It's a regrettable position to be in, because it's nearly impossible to make any long-range plans when you have no idea what the Fed is going to do next. But here we are.

How long the stock market rally will last is therefore unknowable, but stocks and bonds and commodities will remain elevated in price for as long as the Fed continues to dump hundreds of billions of thin-air money into the markets. The only problem is that there's no clear exit strategy for the Fed.

Putting money into the markets is a very easy thing for the Fed to do. Letting rope let out under full sail is easy; tugging it back in is difficult."

www.chrismartenson.com/blog/...-can-party-in-stocks-last/52040

Von daher hier nochmals kurz der Blick auf die zyklisch adjustierten Gewinnerwartungen des S&P500 sowie die POMO-Aktivitäten der Fed.

Wie hier im Thread bereits mehrfach vorgestellt, hat der amerikanische Ökonom Robert Shiller eine Kennzahl entwickelt, die die Kurse nicht mit den aktuellen oder für die Zukunft erwarteten Gewinnen vergleicht, sondern mit jenen, die im Durchschnitt der vergangenen zehn Jahre erzielt wurden. Betrachtet man die Entwicklung dieser CAPE (Cyclically Adjusted Price Earnings Ratio) genannten Kennzahl, so liegt sie bezogen auf die Werte des S&P-500-Index bei knapp 24. Damit ist dieser Markt gemessen am langfristigen Durchschnitt von 16,35 (berechnet ab dem Jahr 1881) zum jetzigen Zeitpunkt bereits deutlich überbewertet.

Was aber nun nicht bedeuten soll, dass dieser Trend durchaus noch exzessiv ausgereizt werden kann, wir sahen dergleichen im Jahr 2000, als man den Anlegern weis machen wollte, dass herkömmliche Bewertungsmaßstäbe nicht mehr zählten. Das Ergebnis ist allseits bekannt.

Desweiteren habe ich einen interessanten Artikel von Chris Martenson mitgebracht, in welchem er sich fragt, wie lange die Party an den Börsen noch weiter laufen könnte. Selbstverständlich kann auch Chris Martenson diese Frage nicht beantworten, nur weist Martenson bei der Durchleuchtung der aktuellen Situation schon darauf hin, dass die Fed den Markt recht wohlwollend pusht. Hier ein Ausschnitt des Martensonschen Statements bzgl. der auch schon von mir früher hier im Thread angerissenen marktstützenden POMO-Aktivitäten der FED:

"As an aside, I used to track the Fed's thin-air money programs very closely, and if you had told me as recently as three years ago that the Fed would have been running 11-figure POMO operations each and every month, I would have told you it was unthinkably impossible. But here we are, that is exactly what is happening, and I am largely numb to the process, which worries me somewhat, as it means that my baseline has shifted.

At any rate, the point here is that from those August lows to now, retail investors have taken out far more money from the stock market than they've placed back in; a total of around minus $38 billion.

But over that same period, the Fed has placed nearly an entire order-of-magnitude more thin-air money, some $350 billion dollars, into the hands of financial institutions, some of whom consider the stock market their personal playground.

Here's a chart of the cumulative POMOs by the Fed from the end of August 2010 to now.

Should we consider the injection of more than a third of a trillion dollars and a stock market that is up by 20% to be a coincidence? No, not in the least. The stock market has become, if anything, a liquidity gauge first and a discounting machine second. The fundamental that matters most is how much money is flowing into the machine.

So it is my view that the trillions of dollars of thin-air money and deficit spending are finally finding their mark (asset prices) and doing their work, just as I predicted they would. Where some called for deflation to be the irresistible force that would drag us all down, I've consistently leaned towards the side of inflation…..

….The old saying is, Don't fight the Fed. That's good advice. I have dutifully been following the developing story by watching what the Fed does, not what it says, and by letting prices tell me which way the wind is blowing. It's a regrettable position to be in, because it's nearly impossible to make any long-range plans when you have no idea what the Fed is going to do next. But here we are.

How long the stock market rally will last is therefore unknowable, but stocks and bonds and commodities will remain elevated in price for as long as the Fed continues to dump hundreds of billions of thin-air money into the markets. The only problem is that there's no clear exit strategy for the Fed.

Putting money into the markets is a very easy thing for the Fed to do. Letting rope let out under full sail is easy; tugging it back in is difficult."

www.chrismartenson.com/blog/...-can-party-in-stocks-last/52040

(Verkleinert auf 97%)

Bubbles are normal and non-bubble times are depressions!